Introduction

In an era of market volatility, technological disruption, and evolving customer expectations, corporate leaders face mounting pressure to allocate resources effectively while delivering superior shareholder returns. Traditional strategic frameworks often lack the granularity to link operational performance and strategy directly to financial outcomes, leaving firms vulnerable to misaligned investments or missed opportunities. This article presents the value creation strategy (VCS) Framework, a novel, empirically

grounded approach that addresses these challenges by categorizing business opportunities into six “Lean versus Grow Archetypes” based on their value creation potential. We have found establishing archetypes to map and guide strategic decision-making offers five key benefits:

- Clarity and focus: Archetypes simplify complex investment options into recognizable categories. For instance, labeling a high-risk tech venture as an “Emerging Growth Engine” clarifies its strategic role.

- Better resource allocation: By prioritizing archetypes aligned with strengths and risk tolerance, firms optimize capital deployment. A “Lean Cash Machine” initiative might receive adequate

reinvestment to sustain efficiency, while a “Thriving Value Leader” warrants significant growth funding. - Risk management: Archetypes highlight risk-return profiles, enabling portfolio balancing. For example, offsetting “Emerging Growth Engine” investment risks with “Lean Cash Machine” stability.

- Consistency in decision-making: The repeatable framework reduces impulsive choices, ensuring alignment with long-term strategy.

- Strategic storytelling: Archetypes translate data into compelling narratives, simplifying communication with stakeholders. A “Comeback Contender’s” turnaround story can rally investor support.

However, archetypes are often established through a subjective qualitative process that can be inconsistent over time. Although they can still be very useful, their value is greatly enhanced

when complemented with an archetype that is fact-based where attributes are quantifiable and objectively observed.

The VCS Framework applies the “Lean versus Grow Archetype” to categorize opportunities, not only on whether they create value, but also how they will create value. The use case for this framework applies broadly to any strategic resource allocation decision, whether it is to decide on where to invest human, physical, or financial capital in a corporate portfolio of initiatives, business units, market segments, products, or customers, or a portfolio of publicly traded stock investments. As means of

demonstrating our framework, we have analyzed 678 companies from the S&P 900, spanning diverse industries and business models (excluding financials and real estate). Covering a 10-year period

from Q1 2014 to Q3 2024, our analysis incorporates 21,167 yearly observations across 32 rolling 3-year periods (20,660 observations), capturing short-term tactics and long-term trends across economic cycles. By focusing on Residual Cash Earnings (RCE) Trend—a composite metric of Growth Contribution and Efficiency Improvement—we establish a clear link to total shareholder returns (TSR), enabling firms to prioritize investments that drive top quartile performance.

The six archetypes—Thriving Value Leader, Emerging Value Leader, Lean Cash Machine, Comeback Contender, Emerging Growth Engine, and Bold Pivot—provide a classification system that informs where a portfolio of assets or strategic initiatives are in the investment cycle. These archetypes simplify strategic planning by offering clarity, improving resource allocation, enhancing risk management, ensuring decision-making consistency, and facilitating compelling strategic narratives. This article details the methodology, results, practical applications, and benefits of the VCS Framework, offering corporate leaders a powerful tool to navigate complexity and meet short-term demands while creating long-term value. Moreover, the proposed archetype also acts as a sanity check against already established qualitative archetypes that help management gain greater conviction in their assessment of how they are looking at their business.

Methodology

Data and sample

As a way of demonstrating our VCS Framework, we analyzed a sample of 678 companies from the S&P 900, excluding financials and real estate to ensure diverse business models and market exposures. The dataset spans Q1 2014–Q3 2024, encompassing various business cycles, sector peaks, and troughs. We employed 32 rolling 3-year periods, each advancing one quarter from Q1 2017, resulting in 20,660 observations. Three-year periods align with typical investor expectations and strategic planning cycles, balancing short-term performance with long-term strategy.

Metrics and strategic questions

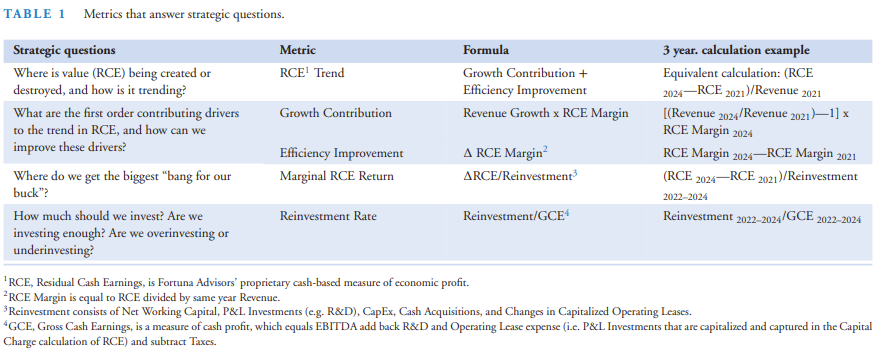

The VCS Framework is built on a set of metrics designed to answer critical strategic questions about value creation, as shown in Table 1. RCE Trend answers the question of where value is being created or destroyed. Growth Contribution and Efficiency Improvement answer the question of how value is being created and/or destroyed, providing clues and guidance on the strategy one should take.

The other measures listed in the table (i.e., Marginal RCE Return and Reinvestment Rate) guide us on how much value we will create per dollar of investment (our “bang for our buck”) and how much we should invest or the rate of investment we should make.

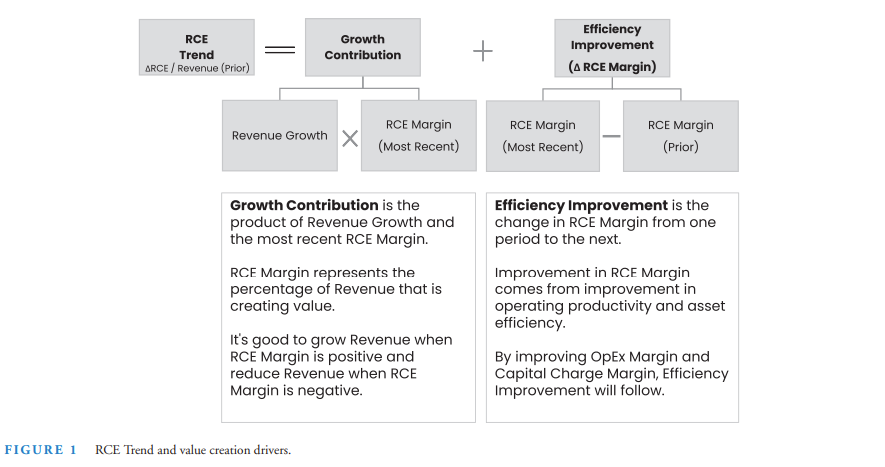

The primary metric is RCE, Fortuna Advisors’ proprietary cash based measure of Economic Profit / EVA (Economic Value Added), which is strongly correlated to total shareholder returns1. RCE Trend can be calculated directly by measuring the change in RCE divided by prior year Revenue. This can be measured monthly, quarterly, annually or over any time period, such as 3 years, as in our study and the example shown in Table 1. Alternatively, it is also the sum of two other measures: Growth Contribution and Efficiency Improvement (Figure 1).

A positive or negative RCE Trend indicates whether value is being created or destroyed, while Growth Contribution and Efficiency Improvement reveals the first-order factors that are driving the RCE Trend. These 3 metrics allow management to visually map these strategies based on a 2 × 2 matrix and set the foundation for establishing a fact-base methodology for creating strategic Archetypes.

Archetype development

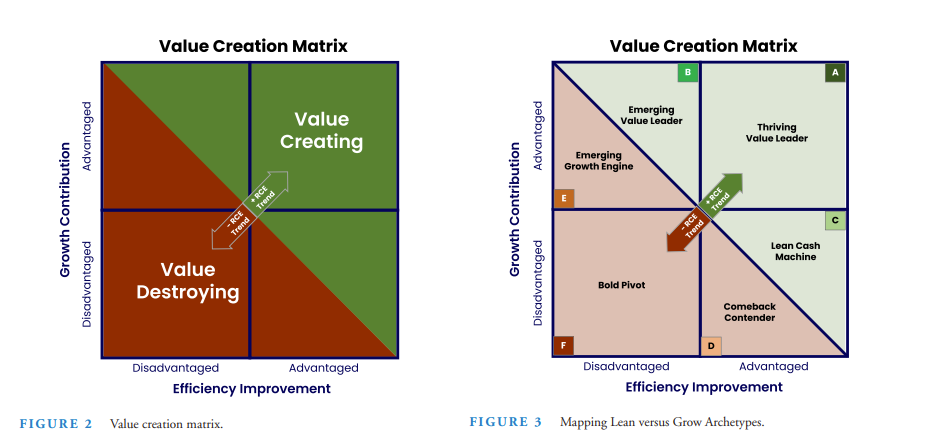

Archetypes were derived by plotting RCE Trend against TSR, identifying clusters that explain performance variations. The Value Creation Matrix decomposes RCE Trend into Growth Contribution and Efficiency Improvement, ensuring Mutually Exclusive, Collectively Exhaustive (MECE) categorization. The matrix, illustrated in Figure 2, maps opportunities along these dimensions, with a diagonal line representing zero RCE Trend. All investments or activities that fall to the right of the diagonal indifference line are value creating and those that fall to the left are value destroying. The indifference diagonal line is where an investment is generating a return on incremental investment equal to the cost of capital, thus meeting shareholder expectations. The indifference line plays an important role in discerning whether an investment that falls in the top left or bottom right quadrant is making value creating or destroying trade offs between Growth Contribution and Efficiency Improvement.

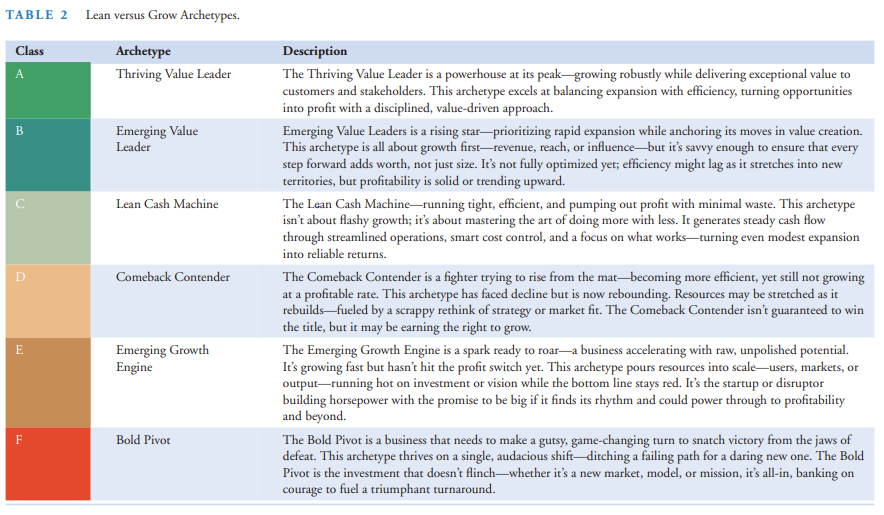

Although there are eight possible combinations of positive and negative RCE Trend, Growth Contribution, and Efficiency Improvement variations, we narrowed them down to the six quadrants as shown in Figure 2. We then categorized each quadrant by the attributes most commonly found and designated an archetype that described those opportunities based on their attributes of RCE Trend, Growth Contribution, and Efficiency Improvement. Table 2 provides the name of each archetype and a description for what we refer to as the “Lean versus Grow Archetypes”.

Figure 3 shows where these “Lean versus Grow Archetypes” are mapped quantitatively on the Value Creation Matrix, providing an intuitive sense of which opportunities have created the most and least value and whether they achieved it through Growth Contribution, Efficiency Improvement or both.

The top right and bottom left quadrants of the Value Creation Matrix consist of the Thriving Value Leader which generates value from both dimensions of Growth Contribution and Efficiency Improvement, while Bold Pivot opportunities destroy value from both dimensions.

The top left and bottom right quadrants are less obvious, where there is a trade-off between Growth Contribution and Efficiency Improvement. In the top left quadrant, the Emerging Value Leader is creating value because the positive Growth Contribution is outpacing the negative Efficiency Improvement. The Emerging Growth Engine is destroying value because the positive Growth Contribution is not enough to offset the negative Efficiency Improvement. In the bottom right, the Lean Cash Machine continues to create value because the positive Efficiency Improvement outweighs the loss in Growth Contribution. Meanwhile, the Comeback Contender’s positive Efficiency Improvement is overshadowed by the loss in Growth Contribution.

Intuitively, one would think that on average, those opportunities that create positive RCE Trend would reflect higher market value changes than those opportunities that produced negative RCE Trend. One might also hypothesize that a Thriving Value Leader that had positive RCE Trend due to both positive Growth Contribution and Efficiency Improvement would yield the highest changes in market value, while a Bold Pivot opportunity that generated negative RCE Trend, Growth Contribution, and Efficiency Improvement would create the least changes in market value. We decided to test our intuition by using publicly available information from a sample of 678 companies from the S&P 900, excluding financial and real estate companies.

Results

Empirical relationship

To verify if our “Lean versus Grow Archetypes” intuition held true, we analyzed 21,167 observations from 678 companies over 32 rolling 3-year periods (20,660 observations), starting from Q1 2017 and advancing one quarter at a time. We compared the median 3-year Total Shareholder Return (TSR) to the 3-year RCE Trend for companies within each archetype. Figure 4 summarizes the results, illustrating the positive correlation between RCE Trend and TSR, where archetypes that generate positive RCE Trend (Thriving Value Leader, Emerging Value Leader, and Lean Cash Machine) do better than archetypes that generate negative RCE Trend (Comeback Contender, Emerging Growth Engine, and Bold Pivot). We also confirmed our hypothesis that a Thriving Value Leader, with a positive RCE Trend driven by both strong Growth Contribution and Efficiency Improvement, would achieve the highest increases in market value. Conversely, a Bold Pivot opportunity, characterized by negative RCE Trends, declining Growth Contribution, and Efficiency Improvement, would result in the smallest changes in market value.

What was most interesting and instructive, is that when an archetype generates positive RCE Trend, forgoing Efficiency Improvement for greater positive Growth Contribution (i.e., Emerging Value Leader) resulted in higher TSR than forgoing Growth Contribution for greater Efficiency Improvement (Lean Cash Machine), despite having virtually the same RCE Trend. This would suggest that when RCE Trend is positive, stepping on the pedal and investing in more growth will generate more market value than investing in efficiency improvement. However, this is not the case when RCE Trend is negative. Comeback Contender, which produced positive Efficiency Improvement but higher levels of negative Growth Contribution, produced greater market value than Emerging Growth Engine, which produced a positive Growth Contribution that was more than offset by negative Efficiency Improvement. This suggests that when RCE Trend is negative prioritizing Efficiency Improvement is more important. Intuitively, this makes a lot of sense. Growing unprofitable businesses will simply make you more unprofitable faster. Obviously, in certain stages of an opportunity’s life cycle (i.e., start-up), this might not be optional. However, the objective should be to drive Efficiency Improvement as soon as possible and not try to simply grow for growth’s sake or grow yourself to profitability.

Applying the VCS framework

The VCS Framework is versatile, applicable for investors evaluating a portfolio of stock or a company evaluating a portfolio of business units, market segments, customers, and/or products. Each archetype can guide management towards distinct investment strategies depending on the context of an opportunity. By example:

- Thriving value leader: Don’t become complacent. Invest in balanced growth and efficiency, for example, expanding market share while optimizing operations.

- Emerging value leader: Step on the pedal by prioritizing revenue growth with disciplined value creation, such as entering new markets with capital discipline.

- Lean cash machine: Continue to focus on efficiency, streamlining operations to maximize cash flow, but consider whether it is being starved of capital, where growth might be revived through additional investment.

- Comeback contender: Leverage the momentum achieved through Efficiency Improvement, but begin thinking of repositioning and market realignment.

- Emerging growth engine: Scale aggressively, accepting short-term losses for long-term market dominance, typical of tech startups. However, don’t grow for growth sakes. Be relentless in striving for Efficiency Improvement and ensure short-term losses are short-term.

- Bold pivot: Execute transformative shifts, such as entering a new industry or overhauling the business model. Half measures will not be good enough. Bold initiatives need to be taken with pace and discipline.

By mapping opportunities to these archetypes, firms can align investments with strategic goals, market dynamics, and customer needs. For example, a technology company might classify its AI division as an Emerging Growth Engine, directing resources to scale while monitoring RCE Margin to ensure future profitability.

Case Studies

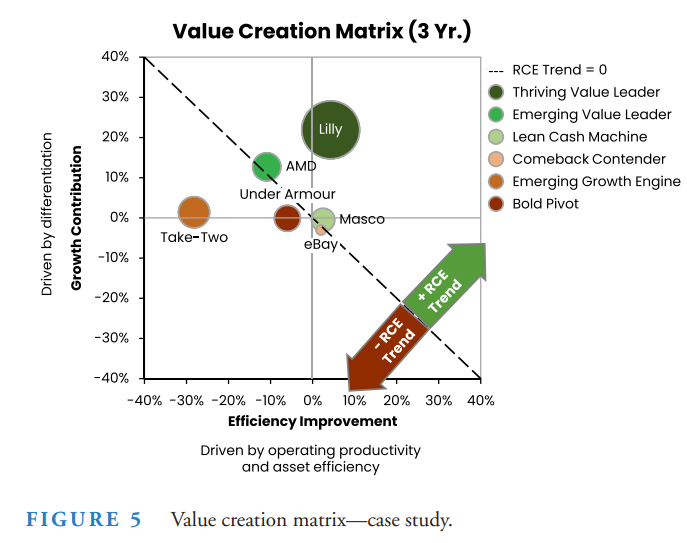

The following case studies, drawn from the S&P 900 Index, offer real-world examples of each archetype, highlighting the key strategies that drove their outcomes. Figure 5 assigns each of the six featured businesses to one of the six archetypes, based on their RCE Trend, Growth Contribution, and Efficiency Improvement metrics over the rolling 3-year period from November 30, 2021, to November 30, 2024.

Thriving value leader: A pharmaceutical powerhouse

Eli Lilly and Company epitomizes the attributes of a Thriving Value Leader, growing robustly while delivering exceptional value through balanced expansion and efficiency in pharmaceutical innovation. Lilly achieved a 26.2% RCE Trend and 56.1% TSR CAGR, driven by a 21.9% Growth Contribution (reflecting strong revenue momentum) and 4.3% Efficiency Improvement from operational enhancements, with a Revenue 3-year CAGR of 13.8% as the company scaled from approximately $27.7 billion to around $40.8 billion by 11/30/2024, propelled by blockbuster incretin-based therapies like Mounjaro and Zepbound amid surging demand in diabetes, obesity, and related indications. This performance stemmed from a multifaceted strategy emphasizing therapeutic diversification into oncology, neuroscience, and immunology; aggressive manufacturing investments exceeding $50 billion by early 2025 (expanding U.S. facilities in Indiana and Wisconsin, plus global sites in Ireland and the U.K.); and an acquisition-driven business development approach (e.g., Morphic Therapeutics for immunology, SiteOne for pain, and Verve for cardiovascular, focusing on early-stage assets to accelerate R&D). Pipeline advancements included eight new Phase III programs in 2024, innovative trial designs, and collaborations like OpenAI for antimicrobials, while global expansion targeted markets like China, Brazil, and Europe with new indications (e.g., sleep apnea and heart failure) and tools like KwikPen to optimize pricing. Efficiency gains arose from market segmentation, disciplined pricing, direct-to-consumer channels like LillyDirect, and a science-driven culture fostering talent and reinvestment in R&D.

Emerging value leader: A fast-growing semiconductor business

Advanced Micro Devices, Inc. (AMD), an Emerging Value Leader, prioritized rapid expansion anchored in value creation through its transformation into an AI and high-performance computing powerhouse. AMD achieved a 1.7% RCE Trend and 17.8% TSR CAGR, driven by a 12.7% Growth Contribution (reflecting robust revenue scaling) partially offset by a −10.9% Efficiency Improvement amid heavy investments. With a Revenue 3-year CAGR of 17.8%, the company grew from $14.8 billion to $24.3 billion, fueled by surging demand in data center AI and diversified computing solutions. This performance stemmed from a strategic pivot under CEO Lisa Su to become an end-to-end AI leader, emphasizing three priorities: a broad portfolio of adaptive hardware/software, ecosystem partnerships, and scaled AI deployments, targeting a $500 billion AI accelerator market by 2028. Strategic acquisitions and partnerships enhanced the companies capabilities, alongside energy efficiency goals as a competitive differentiator. Despite efficiency lags from restructuring (4% workforce reduction in late 2024, $186 million charges to align with AI/enterprise growth) and OpEx increases for R&D/go-to-market, RCE Trend still trended positively.

Lean cash machine: An efficient home improvement and building products company

Masco Corporation exemplifies the Lean Cash Machine archetype, running tight and efficient to generate steady cash flow through streamlined operations and smart cost controls, with minimal waste offsetting modest decline in revenue into reliable returns. Masco achieved a 2.0% RCE Trend and 9.7% TSR CAGR, driven by a −0.5% Growth Contribution (reflecting slight revenue contraction) offset by a 2.5% Efficiency Improvement from productivity initiatives, with a Revenue 3 year CAGR of −1.4% as the company declined from $8.2 billion to $7.9 billion amid volatile repair and remodel markets, yet maintained resilience through operational discipline. This performance stemmed from a consistent strategy emphasizing core business potential in plumbing and decorative products, leveraging enterprise synergies in supply chain, digital transformation, and pricing; active portfolio management via divestitures (e.g., Kichler in 2024) and bolt-on acquisitions targeting 1%–3% annual top-line growth; and diversification beyond China (increased sourcing from Southeast Asia/Mexico) to reduce tariff exposure by 45%. The Masco Operating System (MOS) drove continuous improvements, expanding operating margins from 15.6% in 2022 to 17.5% in 2024 via cost discipline (hiring freezes, reduced spending amid tariffs), volume leverage, and a three-pronged tariff mitigation (price increases, cost reductions, sourcing shifts). With a strong foundation of efficiency, the new CEO seems to be shifting towards a “growth mindset”, emphasizing brand equity and targeted marketing/innovation. Capital allocation is now prioritizing reinvestment towards productivity/innovation and international expansion, enabling flat-to-up sales in 2025 versus declining markets.

Comeback contender: A legacy online auction

eBay Inc. personifies the Comeback Contender, rebounding from decline through enhanced efficiency and a scrappy strategic rethink, though not yet achieving profitable growth at scale. eBay recorded a −1.0% RCE Trend and -4.6% TSR, driven by a −3.0% Growth Contribution (reflecting modest revenue declines amid market challenges) offset by a 2.0% Efficiency Improvement from operational optimizations and targeted investments. Revenue dipped slightly from approximately $11.6 billion in November 30, 2021 to $10.3 billion in November 30, 2024 (a compound annual growth rate of about −4.2%), as the company navigated a slower top-line environment, fueled by a pivot from a broad horizontal marketplace to a focused vertical strategy targeting enthusiasts in core categories like parts & accessories, collectibles, fashion, electronics, and home & garden. Efficiency Improvement gains stemmed from AI investments (e.g., Magical Listing halving seller listing time, adopted by most sellers), geo-specific overhauls, payments partnerships, and a recommerce emphasis. Despite these improvements, analysts noted the need for leadership to prioritize growth.

Emerging growth engine: A software company

Take-Two Interactive Software, Inc. is an Emerging Growth Engine that is accelerating with raw potential through aggressive scaling in mobile and live services, but not yet flipping to profitability amid heavy investments in its pipeline. Take-Two registered a −26.7% RCE Trend and −4.3% TSR CAGR, driven by a 1.4% Growth Contribution (reflecting revenue momentum) significantly offset by a −28.2% Efficiency Improvement from resource-intensive expansions, with a Revenue 3 year CAGR of 17.4% as the company grew from $3.3 billion to $5.4 billion, fueled by mobile acquisitions and recurrent spending despite red bottom lines. Key drivers of growth included the Zynga acquisition in fiscal 2023, adding 15 top-200 U.S. grossing mobile games and boosting mobile and recurrent consumer spending. Investments poured into development, sales, and marketing for flagship innovations, however, the bottom line remained pressured by upfront costs, positioning the firm as a disruptor building for long-term dominance. That said, Efficiency Improvement should be a critical focus to be sure that Take-Two isn’t growing for growth’s sake.

Bold pivot: An apparel company in need of course correction

Under Armour, Inc. exemplifies the Bold Pivot archetype, needing a gutsy, game-changing turn from defeat by ditching failing paths—marked by leadership turmoil, brand erosion, and operational inefficiencies—for a daring new “Underdog Sports House” repositioning. Under Armour recorded a −6.0% RCE Trend and −28.7% TSR CAGR, driven by a −0.1% Growth Contribution (reflecting stagnant revenue) and −6.0% Efficiency Improvement from restructuring burdens, with a Revenue 3 year CAGR of −1.0% as the company declined from $5.6 billion to $5.4 billion, underscoring the urgent need for transformation amid sustained underperformance. This downturn stemmed from interconnected challenges: leadership instability with multiple CEO/product marketing changes creating a “lack of continuity” and “nervous” workforce through layoffs and an “old boys’ club” dynamic limiting diversity; brand dilution shifting from athlete-focused heritage to inconsistent marketing, disconnecting from Gen Z and failing to grow women’s share despite a $1B+ business; product portfolio issues with unfocused assortments (too broad, lacking innovation in footwear/design), pursuing “too many ideas” without franchise architecture; channel missteps via excessive Direct-to-Consumer promotions training consumers for discounts and damaging wholesale relationships by not treating retailers as partners; and poor inventory/forecasting, and pricing pressures from competition/excess inventory. These factors created a downward spiral, necessitating the bold pivot under Kevin Plank’s return (April 2024): declaring a “sports house” identity with underdog grit via logo-centric storytelling and largest marketing investments; optimizing products (25% SKU cuts); rebuilding pricing power (reduced promotions for 10+ point full-price mix); channel reinvention (Direct to-Consumer as brand flagship with higher Average Sales Prices, wholesale to partnerships, $500 M marketing for relevance); operational discipline and significant cuts; leadership additions (three new directors); and regional resets (18-month North America recovery, EMEA growth, APAC full-price focus, India/Southeast expansions). Despite short-term revenue contractions, these audacious shifts addressed root causes, with analysts noting encouragement from promotion reductions/SKU rationalization but emphasizing consistent innovation to inflect growth and change perceptions.

Achieving Top Quartile performance

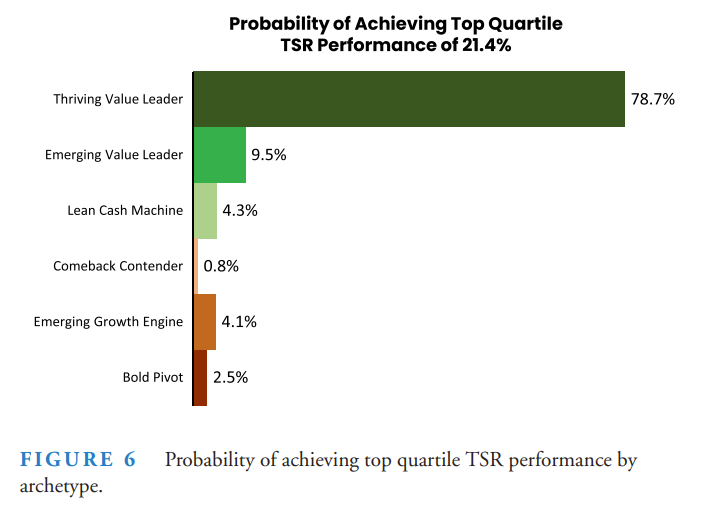

Achieving top-quartile performance is an excellent starting point for aspirational goal-setting, as it inspires greatness while remaining grounded in realistic outcomes. Across our full dataset, the top quartile 3-year compounded TSR stood at 21.4%. That said, merely aiming for this benchmark offers no guidance on how to reach it.

While challenging, this level of return is attainable from any of the six archetypes. Better still, the Value Creation Matrix reveals how to dramatically boost your chances by crafting strategies that emphasize the Growth Contribution and Efficiency Improvement hallmarks of a Thriving Value Leader. As illustrated in Figure 6, Thriving Value Leaders accounted for 79% of all observations delivering top-quartile TSR.

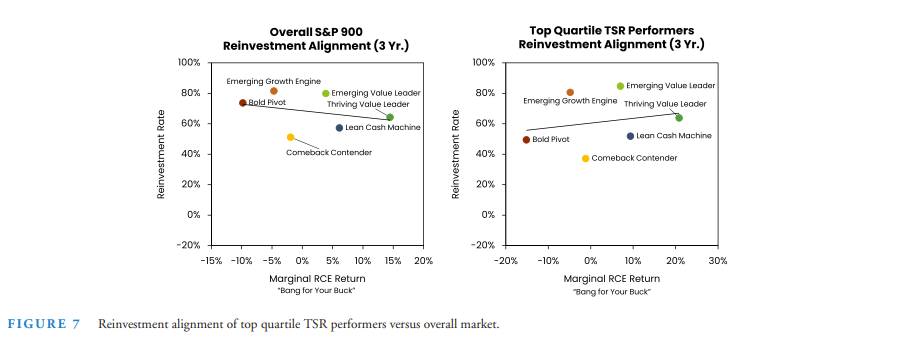

However, transforming opportunities into Thriving Value Leaders through targeted Growth Contribution and Efficiency Improvement strategies is only one side of the equation for top-quartile TSR. Knowing the amount of capital to allocate towards each opportunity plays an equally vital role. To explore this, we charted the median Reinvestment Rate (reinvestment per dollar of Gross Cash Earnings, a cash-based measure of profit) against the Marginal RCE Return (change in RCE per dollar reinvested, or “bang for the buck”) for each archetype.

Figure 7 compares the Reinvestment Alignment for the overall S&P 900 (left) versus top-quartile TSR performers (right). The left chart reflects what we commonly uncover during the initial analysis of a client’s portfolio of investments, where capital is spread thinly—like “peanut butter” across business units, segments, products, and customers. This leads to suboptimal allocation, with more funds flowing into low-value opportunities and less to high-value ones, resulting in a downward-sloping trend.

In contrast, the chart on the right demonstrates a more ideal allocation, contributing to these performers’ success in achieving top quartile TSR. An upward-sloping line indicates that a greater share of profits is reinvested in the highest-value opportunities, maximizing returns per dollar invested.

Conclusion

The VCS Framework effectively connects operational metrics to financial outcomes, serving as a practical tool for corporate leaders. Its MECE archetypes provide thorough coverage of strategic opportunities, bolstered by an empirical foundation that confirms its reliability across diverse industries. This adaptability enables tailored applications, from high-growth tech sectors to mature manufacturing environments.

While rooted in public company data, the framework extends seamlessly to portfolios of privately held businesses, integrating proprietary real-time insights to improve agility amid market changes. Overall, it delivers a robust, data-driven pathway to top-quartile total shareholder returns. By organizing opportunities into six Lean versus Grow Archetypes, it streamlines strategic planning, refines resource allocation, and strengthens stakeholder engagement. Drawing on a decade of S&P 900 analysis, the VCS Framework empowers managers to tackle complexities, mitigate risks, and foster enduring value. In an ever-shifting landscape, it stands as an enduring guide for harmonizing operations with shareholder goals.

How to cite this article: Karame, Marwaan R.. 2025. “A value creation strategy (VCS) framework: Archetypes for achieving top quartile total shareholder returns.” Journal of Applied Corporate Finance 1-8. https://doi.org/10.1111/jacf.12689